- Licensed & Approved Agency in Multiple States

- (888) 901-4870

- (404) 996-0045

Plan F: The Most Popular Medigap/Medicare Supplement Plan F

May 12, 2017

Change Medicare Supplement Plan?

July 22, 2017

Medigap Plan FAQ – Your Questions Answered

What are the “gaps” in Medicare that I might want to cover with a Medigap plan?

A Medigap plan is also known as Medicare Supplement insurance. Medicare Part A and Part B – “original Medicare,” provide important coverage. Part A covers hospital expenses over your deductibles and co-pays, generally about 80%, and Part B provides 80% coverage for most physician’s fees, lab fees, tests, blood, and durable medical equipment. With just Part A and Part B, you will only 80% coverage and my goal for you is to have 100% coverage.

So as you can see, even with Medicare, a medical event could leave you with thousands of dollars of unexpected expenses that would be devastating to someone living on a fixed income.

A Medigap plan is an insurance plan that helps to pay some of what Medicare Part A and Part B doesn’t pay- generally the 20% co-insurance and any Medicare deductibles, so that you don’t have to come out-of-pocket. For example, a Medigap plan covers your hospital deductible per spell of illness or injury ($1,316 as of 2017). There are 11 Medigap plans nationwide to select from, and they all pay a little bit differently.

Do I have to enroll in Part B or Part D to have Medigap Insurance?

You must enroll in both Part A and Part B to buy a Medigap policy. You don’t have to enroll in Part D. However, if you want coverage for prescription drugs, you should consider enrolling in a standalone Part D plan.

Does my Medigap plan cover my spouse?

No. Medigap plans are priced to cover only one person. If you want coverage for you and your spouse you must buy separate Medigap plans and can usually get a discount.

Do I need Medigap if I have Medicare Advantage?

You only need one or the other. You cannot enroll in both plans at the same time. There are advantages and disadvantages to either plan, so speak with an agent and consider your options carefully.

If you currently have a Medicare Advantage Plan, you can enroll in a Medigap plan, but ensure you disenroll from Medicare Advantage before your Medigap benefits begin.

I have a pre-existing condition. Can I get coverage?

That depends. The best time to buy a Medigap plan is during your Medigap open enrollment period. This lasts for 6 months from the day you’re 65, and enrolled into both Parts A and B. During this time you can buy any Medigap plan available in your state, with no health questions asked at all. Plus, coverage for all of your pre-existing conditions. After this time, you would have to answer health questions, and coverage isn’t guaranteed. In addition, if you’re approved, you may pay more.

You can apply for a Medigap plan at any time, and usually if you can answer NO to all the health related questions, you will be approved and have your pre-existing conditions covered. Talking with an experienced agent can help you see if you qualify.

What’s the difference between Medicare Supplement Insurance and Medigap?

There’s no difference. The two terms are interchangeable. However, Medicare Advantage is a different program from both of them.

Does Medigap cover long-term care cost?

No. Generally, all nursing home and custodial care must be paid for out of private savings, via long-term care insurance (ask me about that if you’re interested!) or after all other financial resources are exhausted, by Medicaid. Most people don’t want to be impoverished by long term care costs in order to qualify for Medicaid, so contact me about your options before the need arises.

Does Medigap include prescription drug benefits?

No. If you want this coverage, consider enrolling in Medicare Part D drug plan. An experienced agent can help you find the right plan based on your current medication list. If you don’t take any medications and you don’t sign up when first eligible, you’re subject to a late enrollment penalty.

Can I use my Medigap benefits anywhere in the country?

Yes, you can go anywhere in the country and Medigap works with any physician or care provider that accepts Medicare.

Can I travel abroad?

Yes, most plans will cover 80 percent of medically necessary care while traveling abroad. Not all of them do, though, so make sure to tell your agent that you want this benefit.

When can I enroll in Medigap?

The best time to get a Medigap policy is during the six-month window that starts when you enroll in Medicare Part B, and you’re age 65 or older.

Can I get kicked out of Medigap if I get sick?

No. Medigap policies are guaranteed renewable, no matter how healthy or sick you are. You cannot be disenrolled involuntarily because you are sick. As long as you pay premiums, your Medigap policy will remain in force.

What do I have to pay to a Medicare Supplement insurance agent?

Nothing. The insurance company pays a commission to the agent for bringing you aboard their plan. The agent’s services are free to you. We encourage you to use an agent you trust and who listens to your needs.

What’s the most comprehensive Medicare Supplement plan?

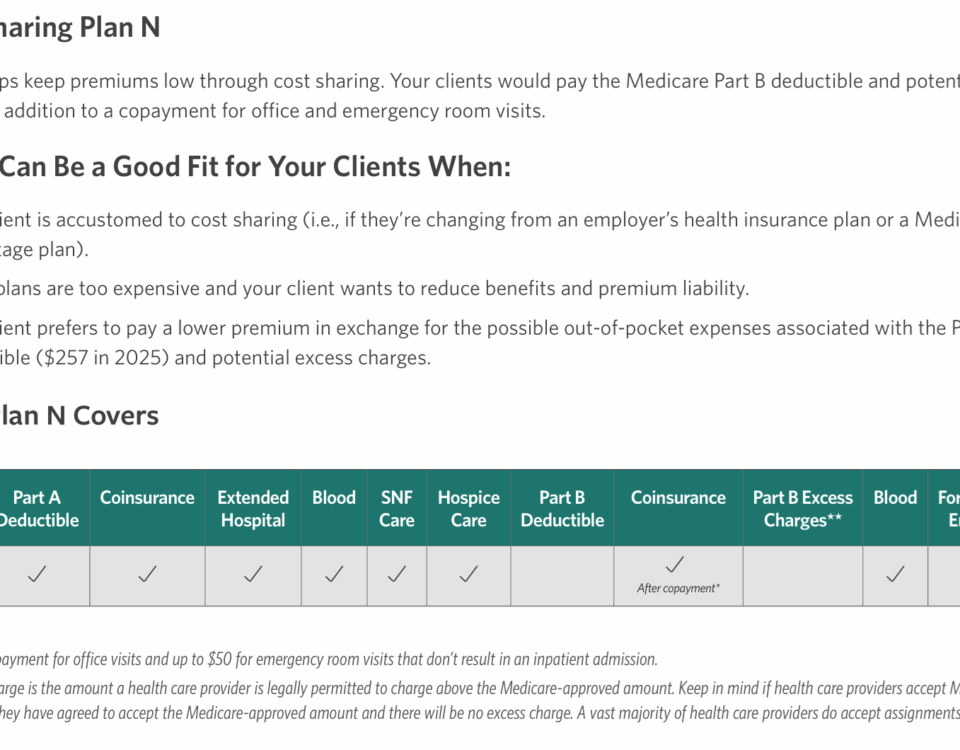

Of the 11 standardized plans available, Plan F provides the broadest coverage, including “first dollar” coverage. That is, in most instances, you won’t have to pay anything out of pocket for anything covered under Part A or B. You also should consider Plan G or even Plan N for lower premiums.

How can I find out more or take the next step?

Call me today! Dial call (888) 901-4870 to reach me, Chad Cason, owner and president of Lifelong Insurance, LLC. We’re a national insurance agency and we work with Medicare beneficiaries from coast to coast on their personal insurance needs, with a particular emphasis and expertise on providing Medicare supplement insurance.

You can also contact me by via my website by clicking on this Contact Us link.

{kind=link}

{kind=link}