- Licensed & Approved Agency in Multiple States

- (888) 901-4870

- (404) 996-0045

2020 Medicare Costs- Your 2 Main Coverage Options

December 30, 2019

Medicare Plan Options Turning 65

April 3, 2020

Turning 65 Medicare Options

This brief article will help you learn more about your turning 65 Medicare options, as well as help you get started with Medicare. You ultimately have 2 choices in how you get your Medicare coverage and there are some important decisions for you to make. Follow these 3 steps to help you get started:

1. Sign up for Medicare through Social Security

If you’re over 65 (or turning 65 in the next 3 months) and not already getting benefits from Social Security, you need to sign up to get Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). You won’t get Medicare automatically.

** Sign up for Medicare online or contact Social Security. Social Security will review your records to see if you qualify for Medicare.

What do I need to know before signing up for Medicare?

Medicare is health insurance for people 65 or older, certain people under 65 with disabilities, and people of any age with End-Stage Renal Disease (ESRD). Your first chance to get Medicare usually starts 3 months before you turn 65 and ends 3 months after you turn 65. However it’s good to start researching early.

You can only enroll in Medicare at certain times, and the cost can go up the longer you wait to sign up. Getting Medicare late can mean lifetime premium penalties and delays in when your coverage can start.

Deciding to enroll in Part B is an important decision. It depends on the type of coverage you have now, and whether you can sign up later (without a penalty). Not all other health coverage is the same as Part B. I can help you know if signing up for Part B at age 65 is best for you, or if you should delay Part B enrollment.

If you’re getting benefits from the Railroad Retirement Board (RRB), you’ll get Medicare Part A and Part B automatically when you’re first eligible. Contact your local RRB office for more information about enrolling in Medicare.

When will I get my Medicare card?

You’ll get your Medicare card in the mail about 2 weeks after you sign up. Your card is included in your official “Welcome to Medicare” packet.

If you already get benefits from Social Security, you’ll get Medicare Part A and Part B automatically when you’re first eligible and don’t need to sign up. Medicare will send you a “Welcome to Medicare” packet 3 months before you turn 65. You’ll still have other important deadlines and actions to take, so read all of the materials in the packet! Call Chad directly at (888) 901-4870 for free help with your turning 65 Medicare options.

2. Choose your coverage

People get Medicare coverage in different ways. You’ll get lots of information to help you make a decision about how to get your Medicare coverage, but it can be very overwhelming! Medicare and even lots of insurance companies will be mailing, calling, emailing with the information below:

- An official “Welcome to Medicare” packet with important information about your coverage options.

- Your official “Medicare & You” handbook once you’re enrolled and every year each fall.

- Information from private insurance companies, agents and brokers (like myself), marketing the Medicare plans they offer. (some of the household names I offer, Aetna, Humana, Anthem, Mutual of Omaha, etc)

To keep it as simple as possible, if you want more coverage than what Original Medicare (Part A & Part B) provides, you have 2 ways or choices to do that.

There are 2 main ways to get Medicare coverage | Turning 65 Medicare Options

Original Medicare – Includes Part A and Part B. You can use any doctor or hospital that takes Medicare, anywhere in the U.S.

- If you want drug coverage, you can join a separate .

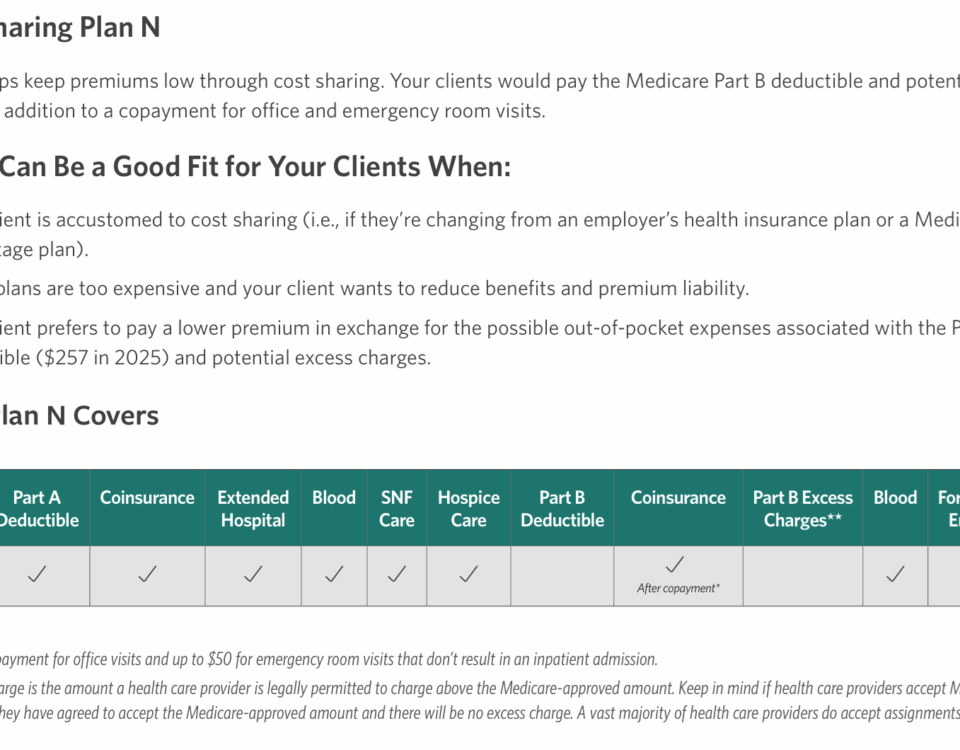

- To help pay your out-of-pocket costs in (like the Medicare Part A hospital deductible & your 20% Medicare coinsurance), you can also shop for and buy like a Medicare Supplement Insurance (Medigap) policy. For example a Plan G or Plan N.

If you don’t enroll into a Medicare Part D or a Medigap policy when you’re first eligible, you may have to pay more to get this coverage later. For Part D, this could mean a lifetime premium penalty.

Medicare Advantage “Part C” – An “all in one” alternative to Original Medicare. These “bundled” plans include Part A, Part B, and usually Part D. Most plans offer extra benefits that Original Medicare doesn’t cover – like vision, hearing, dental, and more. However, your out-of-pocket potential for any hospital and medical related services/procedures could be in the thousands per year.

- Plans require you to be enrolled in Medicare Parts A & B, and you must still pay your Part B premium to Medicare each month.

- Plan premiums for a Medicare Advantage Part C plan can range from $0-100+ per month. In addition to the potential out-of-pocket hospital and medical costs you could incur.

- In most cases, you’ll need to use doctors who are in the plan’s network, or you will pay more or have NO coverage.

3. Need Help?

Just to recap, anything that you see in the mail, t.v, radio, hear from someone who cold called you (even though you’re on the DNC list), ultimately will be a solicitation/product information for a Medigap, Medicare Advantage or Part D Rx insurance plan.

As an independent insurance agent, licensed in many states, I have access to all of the most reputable insurers in your state that offer these plans.

My services as your broker/agent each and every year are free to you. You pay the same rates using an agent like myself for these types of plans as you would going direct with the insurance company.

Direct Line (888) 901-4870!

Turning 65 Medicare Options

{kind=link}

{kind=link}

1 Comment

[…] enrolled in Original Medicare Part A (Hospital 80%) + Part B (Medical 80%) and don’t have group/employer health insurance as an option. In that case, you generally will fall into one of the scenarios below. (Your […]