- Licensed & Approved Agency in Multiple States

- (888) 901-4870

- (404) 996-0045

December 8, 2023

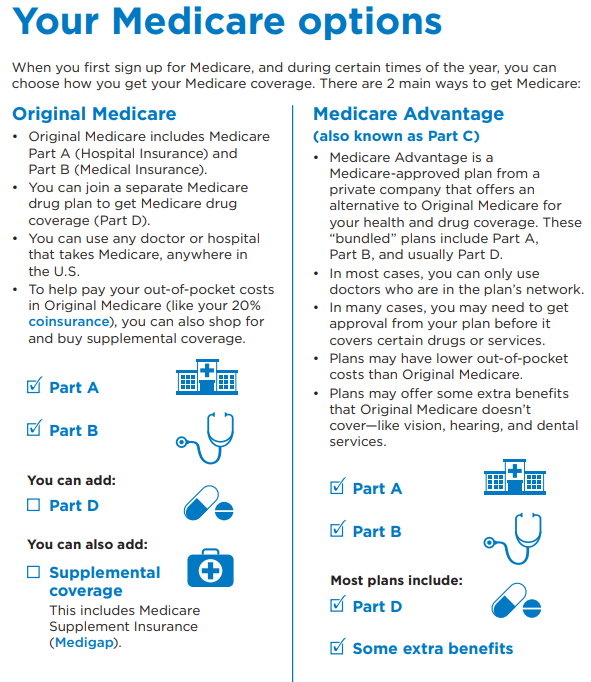

Top Medicare Supplement Questions and Answers As a licensed independent Medicare Supplement (Medigap) agent since 2010, I’ve been asked many questions about Medicare and “supplemental” plan […]

July 18, 2023

Determining the best Medicare plan for you depends on your specific needs and circumstances. Medicare offers several plans, so it’s essential to consider factors such as […]

May 17, 2023

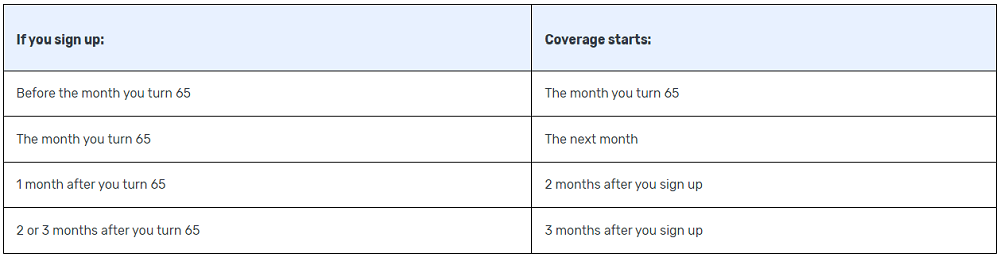

When Does Medicare Coverage Start? Medicare coverage generally starts when you turn 65 and are a U.S. citizen or permanent legal resident who has lived in […]

March 23, 2023

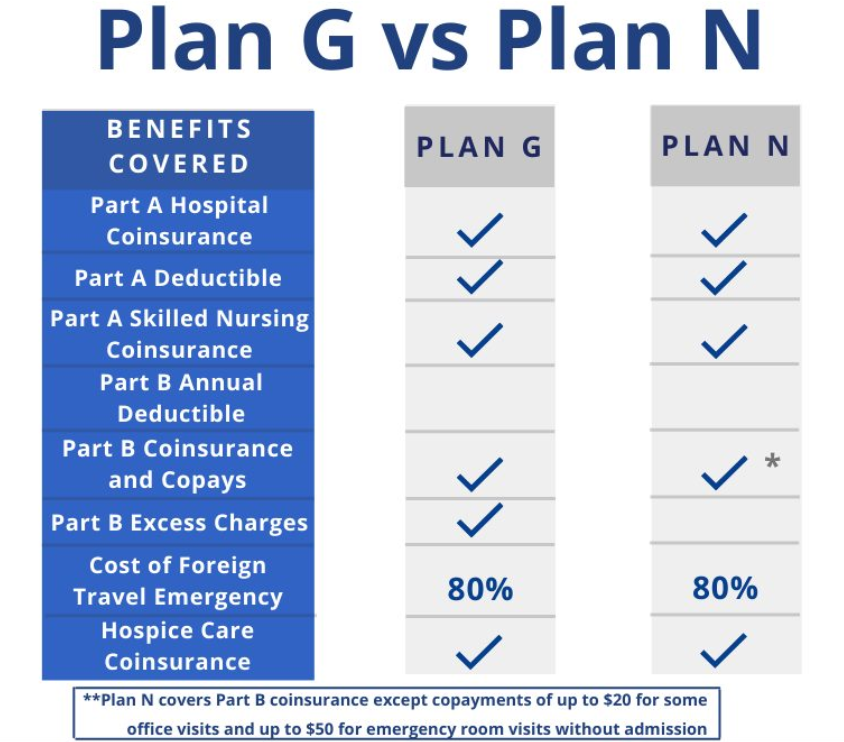

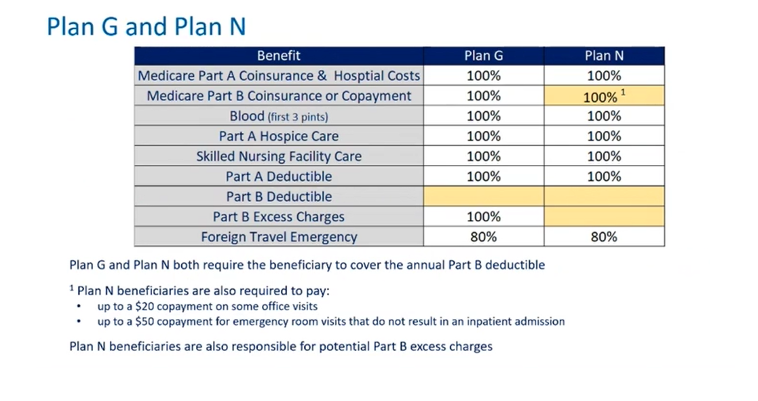

Compare Medicare Supplement Plan G versus Plan N Medicare Supplement (Medigap) insurance plans help pay deductibles and coinsurance Medicare doesn’t cover. In this article, we’ll compare […]

October 22, 2022

2023 Medicare Costs: Parts A & B Premiums and Deductibles One constant thing in life is change, and Medicare is no exception. Here are the 2023 […]

May 16, 2022

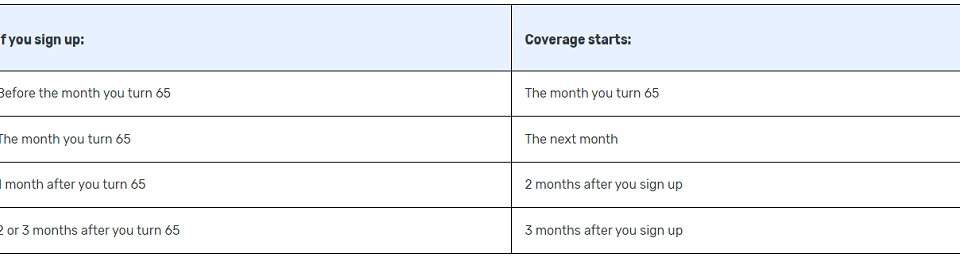

Medicare Part B start date When do Medicare Part A and Part B start? Original Medicare includes Part A (80% Hospital Insurance) and Part B (80% […]

September 22, 2021

Annual Medicare Enrollment The annual Medicare enrollment (election) period runs from October 15th – December 7th. You know it’s that time of year when the Medicare […]

September 8, 2021

What is the Medicare Part B Give Back Benefit? We’ve all seen the commercials with Joe Namath, and now Jimmie Walker “Dyn-O-Mite!”… regarding your Medicare coverage […]

July 14, 2021

{kind=link}

{kind=link}

Why Mutual of Omaha for Medicare Solutions? As an independent insurance agency, I offer many highly reputable companies in the Medicare Market. One of those being […]